The EBA publishes its second MREL impact assessment Report

An Analysis of the EBA MREL Impact Assessment (2022-2024)

1. Overview of the Mandate and Report Scope

This analysis provides a technical review of the European Banking Authority (EBA) report, official reference EBA/REP/2026/06 (March 2026). The document fulfills the mandate established under Article 45l(2) of the Bank Recovery and Resolution Directive (BRRD), representing the second triennial iteration and the final assessment conducted under the current regulatory framework.

The report evaluates the impact of the minimum requirement for own funds and eligible liabilities (MREL) on EU institutions, financial markets, and funding structures during the 2022–2024 reference period. This window reflects the "steady state" achieved following the full implementation of the BRRD II framework. The assessment utilizes data from 345 resolution groups-representing approximately 77% of EU banking sector assets-and a broader sample of 299 banking groups (94% of assets) for the analysis of funding structures.

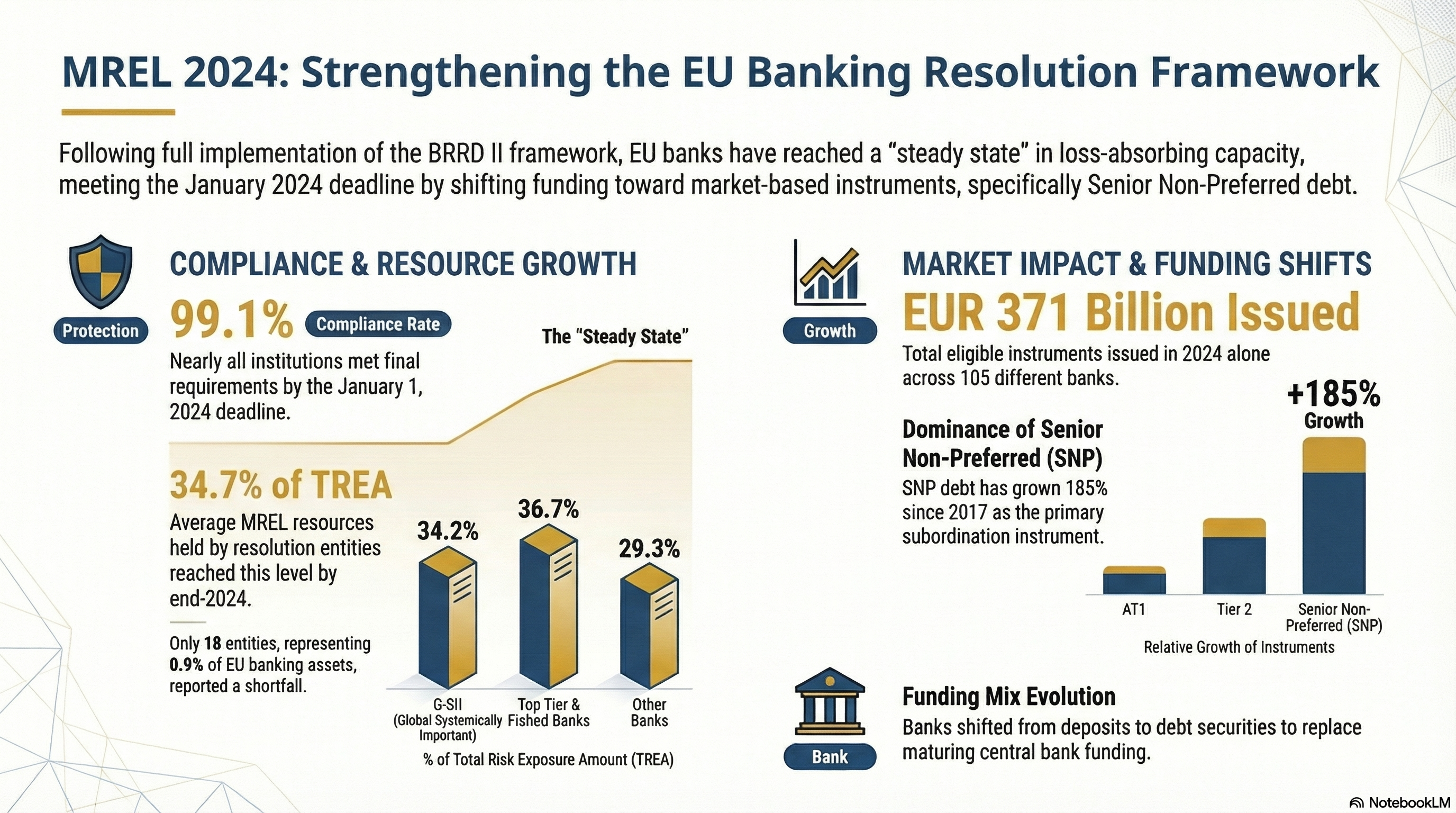

2. Status of MREL Compliance and Requirements

As of the conclusion of the 2022–2024 reference period, a measurable build-up of MREL resources was observed across the Union. Resolution entities reported an average holding of 34.7% of their Total Risk Exposure Amount (TREA) in eligible instruments by end-2024.

The weighted average MREL targets, including the Combined Buffer Requirement (CBR), were recorded as follows for Q4 2024:

- Global Systemically Important Institutions (G-SIIs): 28.9% of TREA

- Top-tier and "fished" banks: 28.4% of TREA

- Other banks: 25.1% of TREA

The regulatory category of "fished" banks refers to resolution entities of smaller resolution groups considered likely to pose a systemic risk in the event of failure, as defined under Article 45c(6) BRRD. Regarding compliance, the EBA reported that 18 entities remained in a shortfall position at the end of the reference period (Q4 2024), accounting for 0.9% of EU banking assets. This figure represents a slight decrease from the 21 banks identified mid-period in the Q2 2024 dashboard. These 18 entities are currently utilizing transitional arrangements as permitted under Article 45m of the BRRD.

3. Evolution of Funding Structures and Debt Instruments

The implementation of MREL is associated with a measurable reallocation in institutional funding strategies. Data indicates a strategic preference for the issuance of Senior Non-Preferred (SNP) debt, which has emerged as the primary instrument for meeting the subordination requirements introduced by BRRD II for G-SIIs and Top-tier institutions. This preference is reported by authorities as a result of the cost-effectiveness of SNP relative to more expensive subordinated instruments like Additional Tier 1 (AT1) and Tier 2 capital.

The following table details the relative change in market values for primary debt types between December 2017 and December 2024:

Debt Instrument Type | Growth/Decline in Market Value (2017-2024) |

Senior Non-Preferred (SNP) | +185% |

Additional Tier 1 (AT1) | +77% |

Senior Unsecured | +76% |

Tier 2 | +4% |

While the long-term trend since 2017 shows growth across most categories, the period following the 2019 entry of BRRD II saw a measurable decline in more expensive instruments; specifically, AT1 and Tier 2 volumes decreased by 6% and 23% respectively between 2019 and 2024, indicating a pivot toward SNP to fulfill MREL subordination mandates.

4. Market Dynamics and Pricing Trends

The yield of eligible debt instruments was influenced by market volatility associated with the COVID-19 pandemic and the interest rate tightening cycle initiated in July 2022. While yields peaked during these periods of stress, a tightening of spreads was observed following September 2023, the pivot point at which the European Central Bank (ECB) commenced rate reductions.

The market demonstrated a consistent perception regarding the risk differential between debt layers. The spread between SNP and senior preferred debt remained stable throughout the reference period, suggesting a clear investor understanding of the hierarchy. Conversely, Tier 2 instruments exhibited higher volatility and a more pronounced sensitivity to market conditions than SNP, particularly during periods of acute market stress.

5. Categorical Impact: From G-SIIs to Smaller Institutions

The capacity to access wholesale markets and the resulting funding strategies vary according to institutional business models and resolution strategies:

- Multiple Point of Entry (MPE) Groups: These entities developed independent capital market access at the level of each resolution entity. Authorities reported successful issuances of SNP, Tier 2, and senior instruments via both private and public placements on domestic and international exchanges.

- Single Point of Entry (SPE) Groups: In contrast to MPE models, subsidiaries within SPE groups reported issuing MREL instruments directly or indirectly to their parent entities.

- Smaller/Retail Banks (LSIs): Less Significant Institutions continued to rely predominantly on equity and Common Equity Tier 1 (CET1) to meet MREL targets. These entities face structural barriers including issuance size requirements, credit rating limitations, and a narrower investor base.

- Local Market Dynamics: In jurisdictions with limited local market depth, the use of "anchor investors," such as development banks, was reported as a mechanism to absorb issuances and foster market confidence.

6. Institutional and Business Model Impact

Resolution and competent authorities reported that structural adjustments within banking groups remained limited and were primarily driven by broader resolvability considerations rather than MREL compliance specifically. The official view among authorities is that there have been no material changes to bank business models or legal structures directly attributable to MREL.

However, the assessment acknowledges that the framework's impact is not uniform. Smaller, deposit-funded institutions face relatively higher compliance costs and greater administrative complexity. In response to these proportionality concerns, the EBA is currently reflecting on Recommendation 9 of the Report on the efficiency of the regulatory and supervisory framework, which evaluates potential methods to streamline capital and MREL requirements for smaller entities.

7. Theoretical Benefits to Financial Stability

The MREL framework serves as a central pillar of the EU resolution regime. The stated objectives of the framework include shifting the burden of loss absorption and recapitalization from public funds to private bail-in debt investors.

The intended outcomes of this shift, as supported by academic literature cited in the report, include:

- Reduction of Moral Hazard: Diminishing the "too-big-to-fail" perception by ensuring private investors bear losses.

- Elimination of Implicit Subsidies: Removing the competitive advantage previously held by systemic banks assumed to have sovereign support.

- Enhanced Market Discipline: The report identifies that reforms have successfully increased the sensitivity of funding costs to bank-specific risk, which is considered a critical metric for institutional accountability and prudent risk management.