Insurance Europe calls on EU leaders to deliver a genuine simplification package for financial services

Europe's Strategic Imperative: The Case for a Financial Services Simplification Package

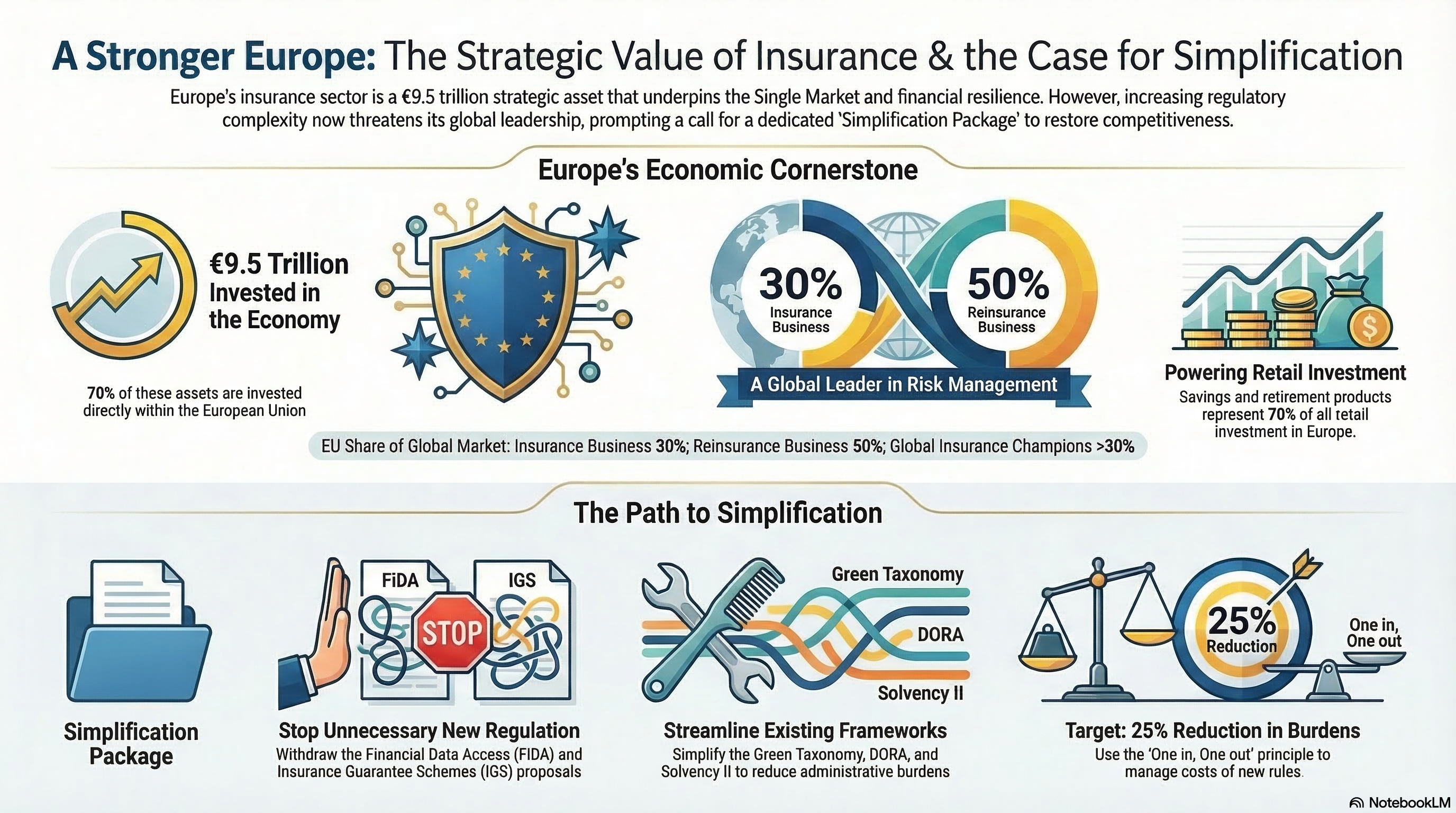

1. The Economic Weight of the European Insurance Sector

In an increasingly fragmented geopolitical landscape, the European insurance and reinsurance sector represents a critical strategic asset, underpinning the Union's long-term financial resilience and the development of a robust Savings and Investments Union (SIU). The sector's capacity to act as a stabilizer for the European economy is evidenced by its immense scale:

- €9.5 trillion invested in the economy: With 70% of these assets held within the EU through equity, corporate bonds, and sovereign debt, the industry is a cornerstone of the Single Market.

- 70% of retail investment: Insurance-based savings and retirement products constitute the vast majority of household capital market participation.

- Global Market Dominance: Europe holds a 30% share of the global insurance business and 50% of the global reinsurance market.

- Home to Global Champions: The EU hosts over 30% of the world's leading insurance and reinsurance firms, providing the patient capital essential for economic autonomy.

By channeling retail savings into productive investment, the sector is fundamental to deepening capital markets and ensuring that European citizens have access to essential pension and protection solutions.

2. The Complexity Crisis: Identifying Regulatory Overlap

The current regulatory environment has reached a tipping point where complexity has become the enemy of progress. The proliferation of overlapping legal frameworks stifles innovation and creates administrative burdens that undermine the very competitiveness the EU seeks to project globally.

To restore balance, European institutions must adhere to the 25% administrative burden reduction target. Central to this effort is the strict application of the "One in, One out” principle to manage regulatory costs and the "Once-Only" reporting principle. The latter requires a structural shift where public authorities exchange verified data and documents directly across Member States, eliminating the need for businesses to submit the same information in multiple formats to different regulators.

Furthermore, we must acknowledge that the 25-year-old Lamfalussy process no longer fulfills its objective of streamlining legislation. Instead, it frequently results in extensive delegations of power to the European Supervisory Authorities (ESAs), shifting key decisions from elected co-legislators to technical rule-making, supervisory convergence, and enforcement. To protect the integrity of political agreements, ESA mandates must be clearly defined and proportionate, preventing technical bodies from reinterpreting the legislative intent. National policymakers also share this responsibility; “gold-plating” must be aggressively curtailed, with any additional requirements strictly justified to prevent the fragmentation of the Single Market.

3. The “Financial Services Omnibus”: Proposed Regulatory Adjustments

Turning political momentum into measurable results requires a “Simplification Package” focused on high-impact priorities, many of which should be consolidated within a Financial Services Omnibus. These adjustments are essential to ensure that regulation empowers rather than hinders the industry's role in the economic recovery.

Priority 1: Halting Unnecessary New Regulation

- Withdrawal of the Financial Data Access (FiDA) proposal: Avoiding new and additional regulation where possible.

- Cessation of minimum harmonization for Insurance Guarantee Schemes (IGS): Not pursuing minimum harmonisation of Insurance Guarantee Schemes.

Priority 2: Streamlining Existing Frameworks

- IRRD “Stop-the-Clock” Reassessment: To reassess scope, proportionality and implementation timelines.

- Solvency II Pillar 2 and 3 Adjustments: Targeted adjustments consistent with the objectives of the simplification agenda.

- Green Taxonomy Reporting: Further simplification of the framework to reduce excessive reporting burdens.

- SME Accounting and Audit Rules: Addressing disproportionate accounting and audit rules, in particular for SMEs.

- DORA Alignment: Avoiding overlaps and reducing bureaucracy.

4. Strategic Reinvestment: The Dividends of Simplification

The ultimate objective of this simplification agenda is the strategic reallocation of capital. By reducing the deadweight of compliance overhead and regulatory duplication, the sector can shift its focus from administrative box-ticking to its primary economic function: the mobilization of long-term investment. This “simplification dividend” is vital for Europe's strategic autonomy and its ability to fund the transition to a modern, secure economy.

Reducing the regulatory burden will allow the insurance sector to more effectively channel patient capital into five strategic priority areas:

- Green and clean technologies

- Innovation

- Defense capabilities

- The energy transition

- Adequate protection for businesses and households

5. Conclusion: A Call for Decisive Leadership

The preservation of European strategic leadership is inextricably linked to the health and competitiveness of its insurance sector. EU leaders have reached a pivotal moment where they must prove that competitiveness is a genuine priority rather than a mere rhetorical device.

As Frédéric de Courtois, President of Insurance Europe, recently stated: “Preserving the strategic leadership of European insurers and reinsurers is preserving Europe's leadership. Every unnecessary rule has a cost, for families, businesses, and the investments Europe urgently needs. European leaders have a real chance this week to prove that competitiveness and simplification are real priorities, not just slogans.”

The insurance and reinsurance industry remains committed to constructive engagement with EU institutions. We stand ready to deliver the investment and resilience Europe requires, provided the regulatory framework is adjusted to support, rather than stifle, our economic contribution.