EIOPA’s Final Report on Solvency II Reporting and Disclosure Amendments

Technical Analysis of EIOPA's Final Report on Solvency II Reporting and Disclosure Amendments

1. Regulatory Context and the Burden Reduction Objective

On 30 March 2026, the EIOPA published its Final Report (EIOPA-BoS-26/081) regarding amendments to the technical standards for supervisory reporting and public disclosure. This report represents the culmination of a regulatory process that included a public consultation launched in July 2025.

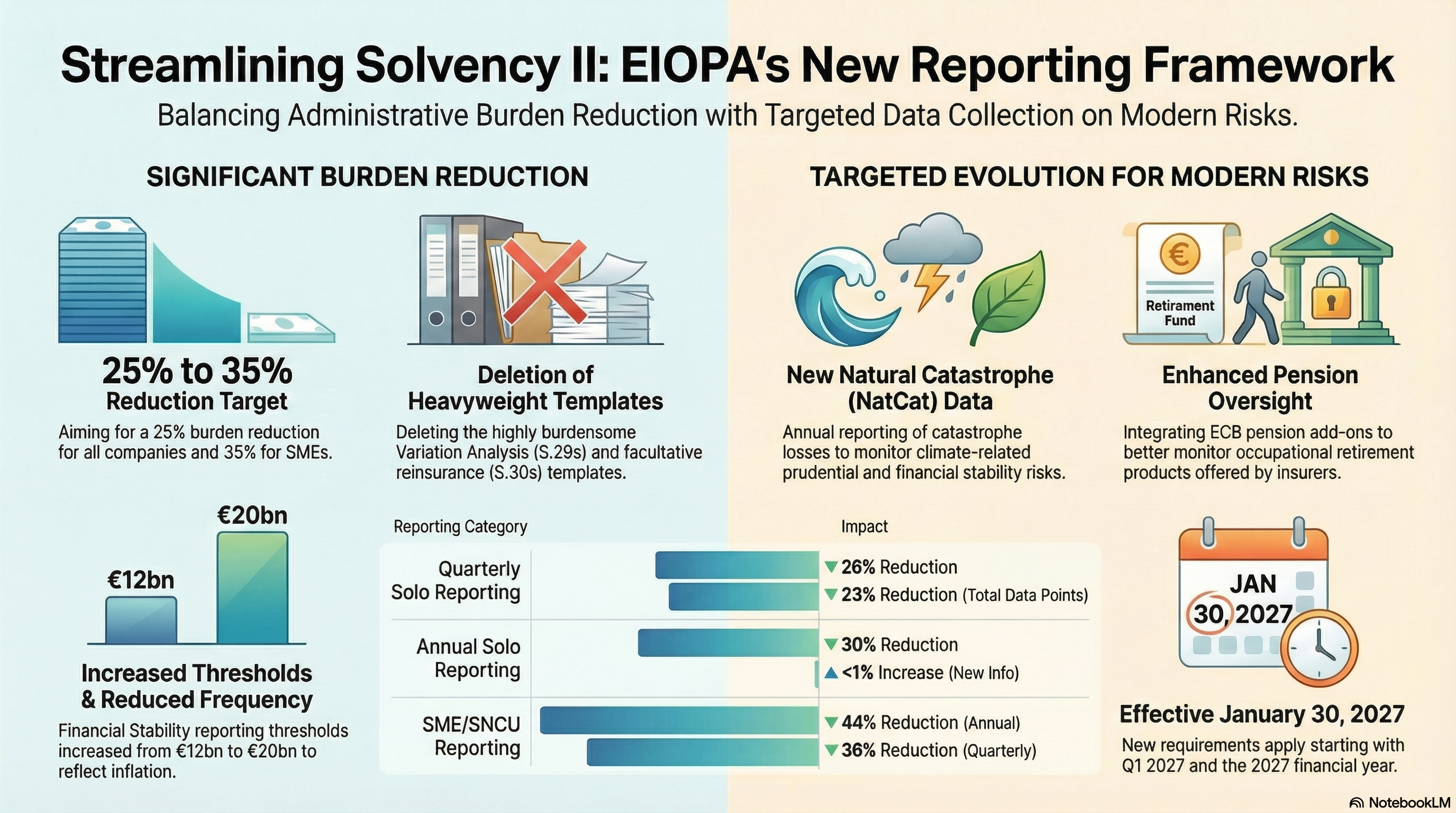

The revisions are fundamentally anchored in the European Commission's (EC) cross-sectoral mandate to streamline the regulatory environment. Specifically, the EC has targeted a 25% reduction in reporting burdens for the general corporate population and a 35% reduction for SMEs by 2029. To achieve these targets within the insurance sector, the report proposes amendments to Implementing Regulations (EU) 2023/894 and 2023/895, alongside a substantial overhaul of the guidelines for financial stability and the supervision of third-country branches.

2. Core Changes Stemming from Solvency II Level 1 and Level 2 Reviews

The technical architecture of several templates has been modified to align with the revised Solvency II Directive and Delegated Regulation. These updates ensure that the reporting framework accurately reflects new legislative mechanisms such as risk-corrected spread adjustments and extrapolation phasing-in.

Key technical adjustments include:

- S.01.02 (Basic Information): Updated with additional columns to facilitate the reporting of adjustments to risk-corrected spreads, the phasing-in of extrapolation mechanisms, and instances of long-term equity breaches of the Solvency Capital Requirement (SCR).

- S.22.01 (Long-term Guarantees): Adjusted to satisfy new disclosure mandates regarding the impact of extrapolation phasing-in.

- S.22.07 (Volatility Adjustment): This new template replaces S.22.06 to accommodate revised calculations for the volatility adjustment and corresponding best estimates categorized by country and currency.

- S.23.01, S.23.04, S.25.01, S.25.05: Revised to reflect matching adjustment (MA) simplifications, specifically the removal of the requirement to report the nSCR of the Matching Adjustment Portfolio (MAP) and the elimination of the requirement to report each MAP separately.

- S.26.01–S.26.07: These templates now incorporate simplified calculations for immaterial sub-modules and risk mitigation. They also reflect updated reporting for defaulted and forborne loans within the counterparty default risk framework and changes to equity investments under specific legislative programs.

- NACE Code Reporting: Instructions for reporting NACE codes have been updated to align with the NACE 2.1 version, which becomes applicable in 2025.

3. Strategic Deletions and Frequency Reductions

EIOPA has executed a strategic contraction of the reporting package by identifying templates where the effort-to-value ratio was suboptimal for routine supervision.

Annual Template Deletions The following templates are slated for deletion based on their high administrative cost and limited supervisory utility:

- Underwriting Risk (S.21 series): S.21.01, S.21.02, and S.21.03 are removed as they generally lacked the granular, undertaking-specific detail required for effective routine oversight.

- Variation Analysis (S.29 series): S.29.01 through S.29.04 are deleted. Industry data indicated these templates could account for up to 50% of the total reporting effort in some instances, yet they frequently failed to provide supervisors with a coherent explanation of asset-liability movements. This deletion represents a significant pivot toward supervisory efficiency over manual labor.

- Facultative Covers (S.30 series): S.30.01 and S.30.02 are deleted because these highly specific risks are better monitored via ad-hoc requests in cases of material exposure rather than via standardized templates.

- Own Funds: S.23.02 and S.23.03 (at both solo and group levels) are removed to reduce redundancy.

Frequency Reductions

- MCR (S.28.01/S.28.02): These shift from quarterly to annual reporting. Quarterly monitoring of the Minimum Capital Requirement (MCR) will be consolidated within the S.23.01 (Own Funds) template.

- CIU Look-through (S.06.03): Reporting is reduced to semi-annual (Q2 and Q4), maintaining the existing 30% materiality threshold.

4. Proportionality Measures for Small and Non-Complex Undertakings (SNCUs)

To better align reporting requirements with the risk profiles of SNCUs and Small and Non-Complex Groups (SNCGs), significant exemptions have been formalized.

For the Q1 and Q3 reporting cycles, SNCUs are now required to submit only three functional templates:

- S.01.01 (Content of submission)

- S.01.02 (Basic information)

- S.23.01 (Own funds)

Furthermore, SNCUs are granted full exemptions from reporting S.06.04 (Climate change-related risks) and the newly introduced Natural Catastrophe data requirements (S.27.02/S.27.03).

5. Integration of New Information Requirements: NatCat and Pensions

While the primary objective is burden reduction, EIOPA has introduced targeted requirements to fill critical data gaps in climate risk and pension monitoring.

- Natural Catastrophe (NatCat) Data: Templates S.27.02 (Loss data) and S.27.03 (Exposure and premium data) have been introduced to monitor insurance exposure and catastrophe losses at the solo level. Life insurers and SNCUs are exempt. Pure reinsurers are required only to report S.27.02, as exposure data for reinsurers is deemed unnecessary within this specific monitoring framework.

- Pension Data: Following an assessment of policy options, EIOPA has integrated ECB "add-ons" into template S.14.01 (Option 1). This is achieved by expanding the closed list of C0102 (Pension entitlements). Critically, this integration allows for the expected discontinuation of the ECB's E.02.16 reporting, thereby eliminating a significant source of redundant reporting.

6. Financial Stability and Third-Country Branch Guidelines

Revisions to these guidelines emphasize the removal of duplicative text and the adjustment of thresholds to reflect current economic realities.

- Financial Stability: The reporting threshold for both groups and solos has been raised from EUR 12 billion to EUR 20 billion. This increase is specifically intended to reflect the effects of inflation since the previous thresholds were established. This shift is projected to reduce the reporting population by 24% for groups and 53% for solos.

- Third-Country Branches: The volume of individual guidelines has been reduced by 36% (from 61 to 39). Deletions primarily targeted guidelines that were redundant duplications of existing Level 1 or Level 2 legislative text.

7. Implementation Timeline and Transitional Provisions

The following table outlines the application schedule for the revised reporting and disclosure framework:

Date | Milestone |

30 January 2027 | Effective date for revised Guidelines and new reporting requirements. |

2026 Annual Reporting | Based on current ITS, though a transitional provision exempts deleted templates from this cycle. |

Q1 2027 Reporting | First quarterly submission cycle under the new requirements. |

2027 (Ongoing) | Launch of a targeted data collection exercise specifically to monitor capital relief effects following the Solvency II review. |

SFCR 2026 (2027 Disclosure) | Disclosures remain governed by the current legal framework. |

SFCR 2027 (2028 Disclosure) | Disclosures must reflect new structures and audit requirements. |

8. Impact Assessment Summary

Quantitative analysis confirms a significant net reduction in the total reporting burden, even after accounting for the introduction of new NatCat and pension requirements.

- Quarterly Reporting: 26% net reduction in templates.

- Overall Package: 22% net reduction in total data points across the combined quarterly and annual package.

- General Population: 33.6% reduction in annual templates.

- SNCU Population: 43.8% reduction in annual templates.

The introduction of NatCat templates represents a modest 4% increase in annual templates, which is substantially offset by the deletion of the S.21, S.29, and S.30 series. These figures demonstrate that the package achieves a substantial decrease in administrative volume while maintaining the integrity of the prudential monitoring framework.