Robust Investment-Driven Insurance Pricing under Correlation Ambiguity

The Ambiguity Advantage: Why the Risks We Can't Quantify Might Be the Most Profitable

1. The "Unknown Unknowns" of the Modern Insurer

For decades, the insurance industry was viewed through a narrow lens: insurers were simple risk-takers, collecting premiums to cover statistically predictable, if unfortunate, events. In the modern era, however, this business architecture has undergone a radical metamorphosis. Today's insurers operate as sophisticated financial intermediaries, positioned at the volatile intersection of underwriting and global capital markets.

At the heart of this transformation lies a phenomenon that Shunzhi Pang terms "correlation ambiguity"-the fundamental "unknown unknowns" regarding how insurance losses and stock market shifts move in tandem. While traditional actuarial intuition suggests that such deep uncertainty should naturally drive premiums higher to compensate for the added risk, recent research into dynamic equilibrium pricing upends this assumption. Counter-intuitively, the inability to pin down these correlations does not always result in a price hike or a loss of utility. In certain regimes, ambiguity is not a cost to be managed, but a stabilizing force.

2. Takeaway 1: Insurers are the New Financial Intermediaries

The shift from a pure protection model to a financial engineering model is the defining evolution of the sector. Insurers now leverage their core underwriting activities to generate "low-cost funds," which are then deployed into capital markets to capture the equity risk premium.

"As insurers increasingly behave like financial intermediaries, they raise large amounts of low-cost funds through underwriting activities and actively participate in capital markets."

Because of this dual role, the "dependence structure"-the correlation between underwriting risks and financial returns-is now the most critical variable in an insurer's toolkit. In this modern context, the insurance price is no longer just a reflection of potential claims; it is a strategic lever used to balance the firm's liabilities against its performance in the capital markets.

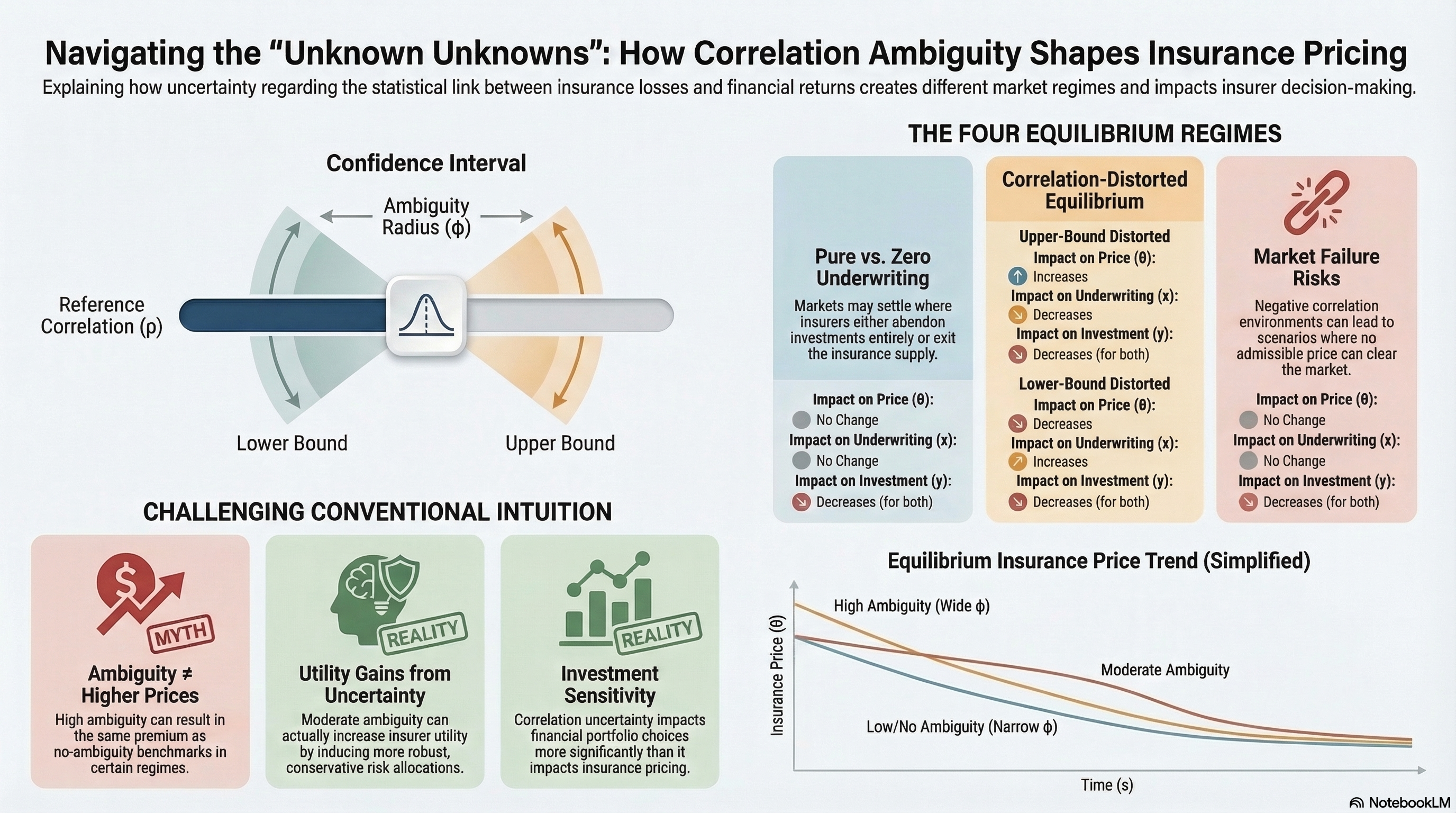

3. Takeaway 2: The Five Faces of Market Equilibrium

The market's response to correlation ambiguity is not a linear adjustment. Instead, behavior is dictated by the profitability ratio (\psi), which compares the gain per unit of underwriting risk (the loading premium \theta l/\eta) to the market's reward for financial risk (the Sharpe ratio). Depending on this ratio and the insurer's level of ambiguity aversion, the market can fundamentally "switch" between five distinct equilibrium regimes:

- Zero Underwriting: The insurance price hits its regulatory upper bound (\bar{\theta}), causing the insurer to exit the underwriting market entirely and move all resources into financial investments.

- Pure Underwriting: The insurer abandons the financial markets, focusing exclusively on insurance activities to avoid unreliable correlation data.

- Upper-Bound Distorted: The insurer remains active in both markets but adopts a robust posture by assuming the maximum plausible correlation (\rho + \phi)-the worst-case scenario for diversification.

- Lower-Bound Distorted: The insurer operates based on the minimum plausible correlation (\rho - \phi), often leading to short-selling or negative investment positions.

- Market Failure: A state where no admissible price can clear the market. This typically occurs when the worst-case correlation (\rho + \phi) falls below a specific threshold (determined by the model's admissibility constraints), making a positive price economically impossible.

4. Takeaway 3: The Price Paradox-Why Ambiguity Doesn't Always Cost You

The most provocative finding from Pang's numerical simulations is the "Price Paradox." In a standard "benchmark" case with no ambiguity, prices follow a predictable path based on historical data. However, as ambiguity increases, insurance prices do not necessarily climb.

In the "Pure Underwriting" regime, the price remains identical to the no-ambiguity benchmark. This happens because high ambiguity triggers a strategic retreat from diversification. When the correlation estimate becomes too "noisy" to trust, the insurer essentially "quits" the financial market to avoid the fragile link between risks. By decoupling investment from underwriting, the price reverts to its fundamental underwriting cost, effectively stabilizing the premium for the consumer.

Interestingly, at a 99% confidence level (representing extreme uncertainty), the insurer's pricing behavior becomes more stable than at moderate levels of ambiguity. At this extreme, the insurer fully commits to the Pure Underwriting regime, preventing the "uncertainty tax" from being passed on to policyholders.

5. Takeaway 4: Finding Strength in the Fog (The Utility Gain)

Conventional wisdom holds that ambiguity is a burden that reduces an insurer's well-being. However, the research reveals a "seemingly counterintuitive finding" regarding utility gains, particularly when dealing with a positive reference correlation (\rho = 0.6).

"A higher degree of ambiguity aversion can increase insurers' instantaneous utility gains."

This occurs because a positive correlation renders traditional diversification "fragile." When an insurer acknowledges the ambiguity of that correlation, they are forced to adopt a more "robust and conservative" risk allocation. By preparing for the worst-case distortion, the insurer endogenously reduces its exposure to correlation-sensitive risk sharing. This defensive posture actually makes the insurer better off, resulting in higher utility gains than if they had blindly trusted a precise-but ultimately incorrect-correlation estimate.

6. Takeaway 5: The Fragility of the "Natural Hedge"

Many risk managers rely on a "natural hedge"-the assumption that insurance losses and market returns will move in opposite directions. However, for those relying on a negative reference correlation (\rho = -0.3), ambiguity poses a significant threat. The research shows that correlation ambiguity "weakens the natural hedging effect," as the worst-case belief often assumes the hedge will evaporate or even flip to a positive correlation exactly when market stress is highest. For the modern strategist, this is a stark warning: the safety net of negative correlation may be a statistical illusion that disappears in the fog of "unknown unknowns."

7. Conclusion: Pricing the Future of Uncertainty

As the industry faces a future defined by volatile climate conditions and systemic catastrophic losses, the correlations between insurance claims and financial markets will only become more elusive. The "unknown unknowns" are the new industry standard.

The insurance industry must now decide if it is ready to move beyond the comfort of "precise but wrong" models. This research suggests that embracing the fog of ambiguity-moving toward "robust but ambiguous" frameworks-is not just a matter of safety. It is a strategic path toward more stable pricing and, surprisingly, higher utility. Are we ready to admit what we don't know to become more profitable?