Insurance Europe: Making the IRRD proportionate, clear and workable before 2027

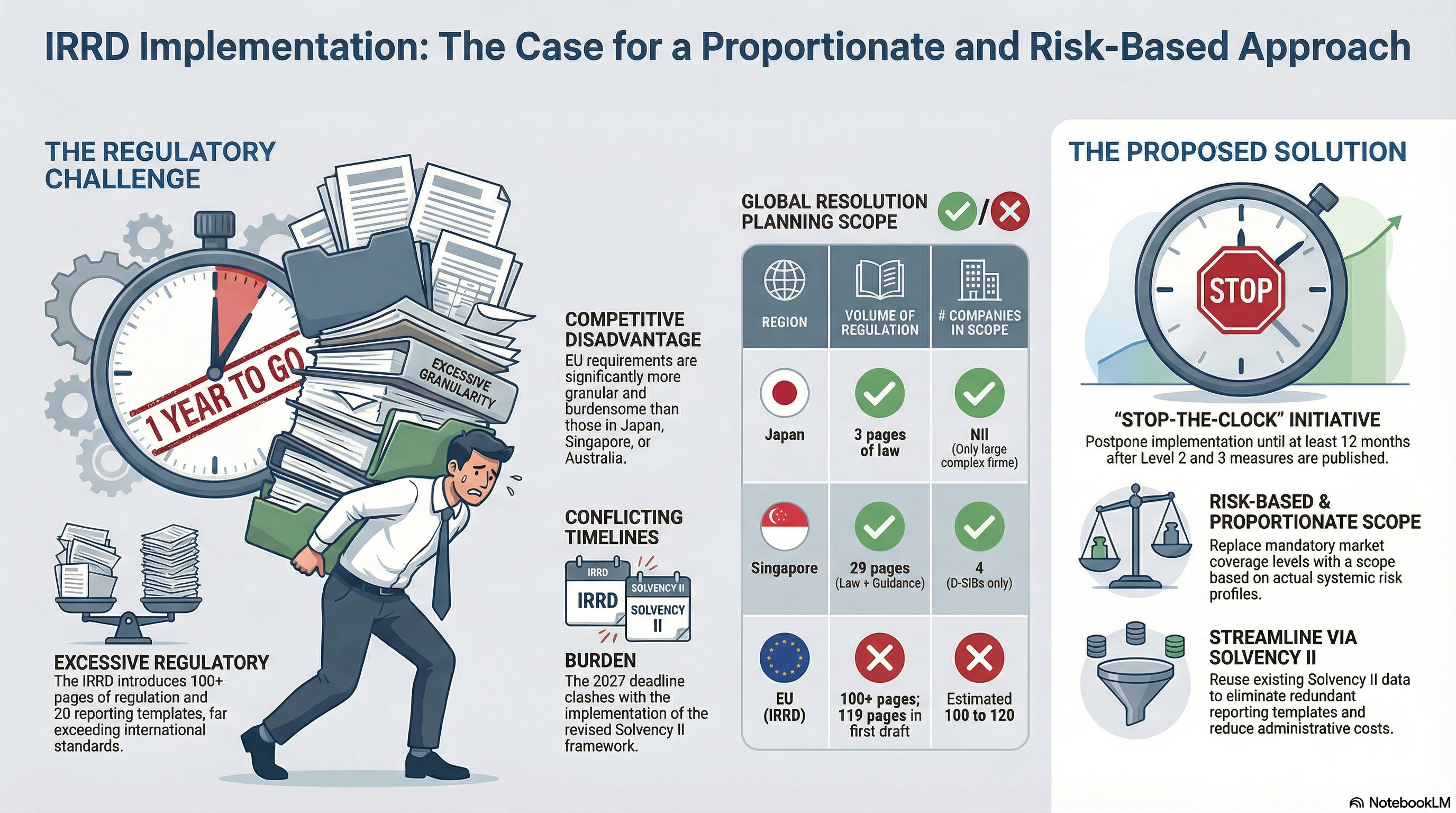

This paper outlines Insurance Europe's critical perspective on the upcoming Insurance Recovery and Resolution Directive (IRRD), which is scheduled for implementation in early 2027. The organization argues that the current timeline is unrealistic due to a lack of regulatory clarity and the absence of finalized technical standards. They contend that the directive imposes excessive reporting burdens and administrative costs that exceed international benchmarks, potentially harming the global competitiveness of European insurers. To mitigate these issues, the paper suggests a "stop-the-clock" initiative to allow for a comprehensive impact assessment and a more proportionate, risk-based approach. The federation specifically recommends phasing in requirements, streamlining documentation by using existing Solvency II data, and refining the definition of critical functions to avoid unnecessary interference with business operations. Ultimately, the text serves as a call for regulatory simplification to ensure the framework remains flexible and focused on genuine systemic risks.

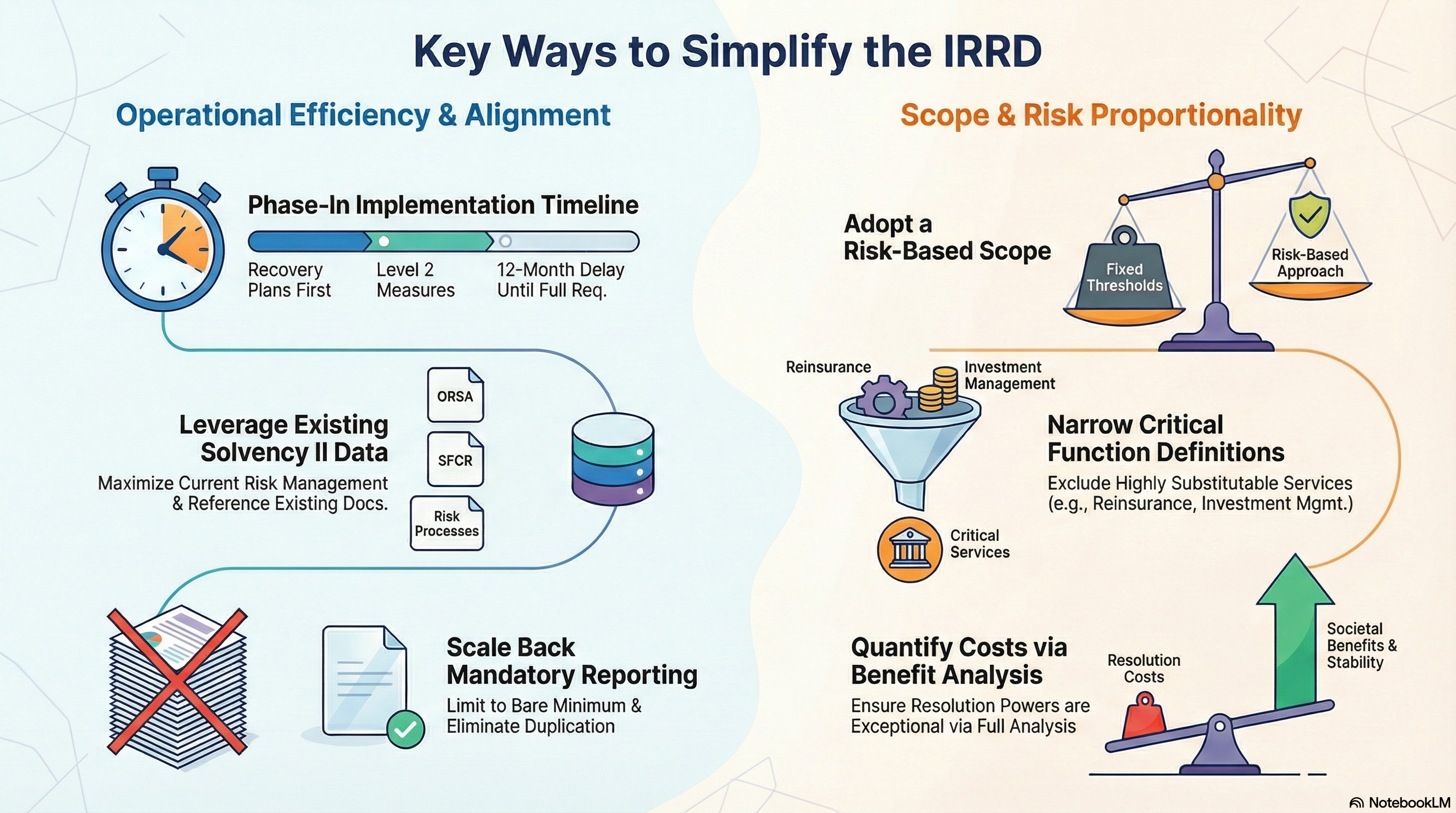

- Postpone the timeline and phase in requirements: The implementation should be delayed until at least 12 months after Level 2 and 3 measures are published to avoid conflicting with the Solvency II review. Requirements should then be phased in, with pre-emptive recovery plans prepared a year before resolution plans.

- Scale back mandatory reporting: Reporting should be limited to the bare minimum and only apply to companies in the scope of resolution planning. This includes deleting templates that duplicate Solvency II data or require market-wide judgments better suited for authorities.

- Clarify and limit the scope of critical functions: Level 2 technical standards should provide clearer, more limited definitions. Highly substitutable services, such as reinsurance, investment management, and actuarial services, should not be classified as critical functions.

- Ensure a risk-based scope: The IRRD should move away from fixed minimum market coverage thresholds toward a risk-based approach. If numerical thresholds remain, subsidiaries already covered by group plans should count toward them.

- Streamline recovery plans: The mandatory content for recovery plans should be reduced, allowing firms to reference existing documents (like the ORSA or SFCR) rather than reproducing information.

- Simplify the resolvability assessment: To avoid a burdensome "tick-box" exercise, requirements for insurers to produce complex playbooks or conduct their own self-assessments should be removed.

- Minimal interference with business as usual: Resolution powers should only be used in truly exceptional circumstances. The immediate costs of using these powers to change business operations must be quantified and considered beforehand.

- Maximise use of existing processes: Implementation should leverage the comprehensive risk management and monitoring processes already established under Solvency II to minimize duplication.

- Perform a full cost-benefit analysis: The administrative burdens and costs of the IRRD should be quantified against expected benefits, taking into account the effectiveness of existing safeguards.

- Ensure appropriate treatment of reinsurance: The Directive should recognize that the cross-border nature of reinsurance is a fundamental part of its value proposition and ensure that the use of reinsurance is not designated as a critical function.