Flood Re: a not-for-profit reinsurance scheme

The Hidden Margin of Climate Risk: Premium Convergence and Coverage Rationing in UK Flood Insurance

1. Contextualizing the Climate Dilemma in Property Insurance

The escalating volatility of physical climate risk presents a fundamental challenge to global property insurance stability. We define this as the "Climate Dilemma": a structural tension between maintaining policy affordability for households and ensuring the continued availability of coverage. As expected losses increase, the protection gap-the delta between total economic losses and insured losses-widens. In 2023, global natural catastrophe losses reached approximately US250 billion, with a staggering US155 billion remaining uninsured. In the UK, the urgency is underscored by 2024 data showing weather-related home insurance claims hitting a record £585 million.

Crucially, recent Environment Agency updates indicate that 4.6 million properties in England are now at risk of surface-water flooding-a 43% increase over previous assessments. When political or regulatory pressure restrains premium growth to preserve affordability, insurers frequently pivot to "quantity rationing," utilizing exclusions or market exits. Our analysis examines how the UK's Flood Re framework-a public–private risk-sharing arrangement-impacts both the pricing and the contractual availability of flood cover, revealing that price stability often masks a "silent retreat" in actual protection.

2. Structural Overview: The Flood Re Framework

Established in 2016, Flood Re is a not-for-profit reinsurance scheme designed to decouple domestic retail premiums from the underlying technical flood risk. The framework allows insurers to cede the flood component of high-risk policies to a subsidized pool.

The scheme's solvency is maintained through three primary funding streams:

- Market-Wide Levy (Levy 1): A compulsory annual charge on all UK household insurers, currently set at approximately £160 million.

- Inward Reinsurance Premiums: Premiums charged to insurers for ceding risk, fixed based on the property's Council Tax band rather than hydrologic hazard.

- Outward Reinsurance: Flood Re's purchase of global reinsurance to cap its own aggregate exposure.

This model provides a sophisticated alternative to the binding rate regulation seen in U.S. jurisdictions like California. Under California's Proposition 103, "intervenors" can challenge any rate increase exceeding 7%, often forcing a reliance on the FAIR Plan (insurer of last resort). Conversely, the UK model uses the reinsurance market to insulate consumers from global price signals, effectively shielding household premiums from the "hardening" global reinsurance cycles.

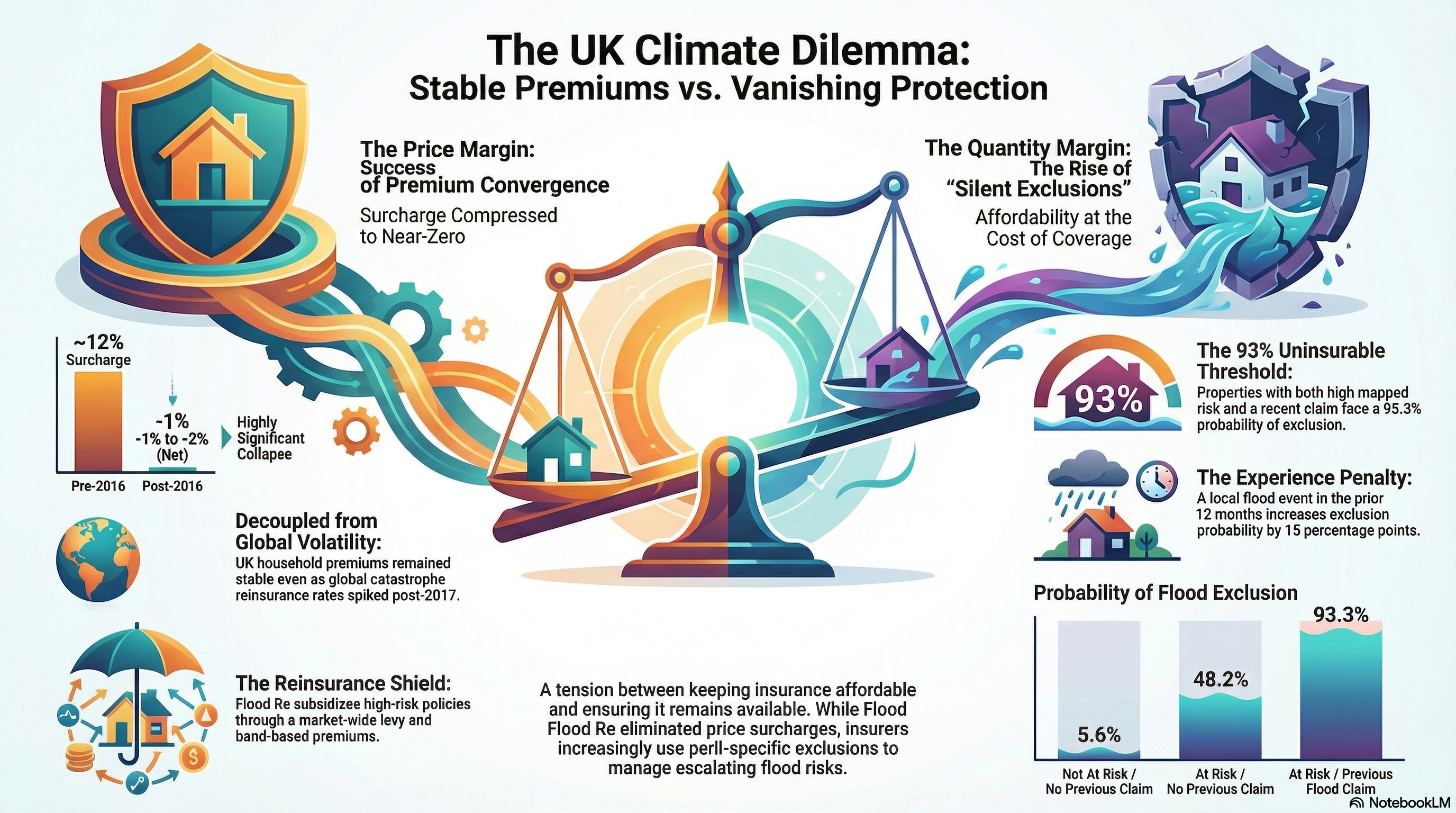

3. Analysis of Premium Dynamics: From Surcharge to Convergence

Our longitudinal analysis of gross written premiums (GWP) proves that Flood Re has effectively eliminated the premium surcharge historically associated with high-risk properties. Before 2016, insurers applied a significant risk-based penalty. Post-intervention, this differential has been compressed to a level that is statistically indistinguishable from zero.

Pre-2016 vs. Post-2016 Premium Differentials

Period | Premium Surcharge (At-Risk Properties) | Statistical Significance |

Pre-2016 | ~12% Surcharge | Highly Significant |

Post-2016 | -1% to -2% (Net Differential) | Statistically Indistinguishable from Zero |

Before the 2022 FCA pricing remedies, the market also exhibited "price walking," with renewals priced approximately 10% higher than new business. Crucially, UK premiums for high-risk zones have successfully decoupled from the Guy Carpenter Global Property Catastrophe Rate-on-Line Index. While global rates spiked post-2017, the UK's subsidized framework allowed domestic premiums to remain stable or even decline in real terms, preventing the transmission of global catastrophe costs to at-risk households.

4. The Extensive Margin: Persistence of Flood Exclusions

While Flood Re has solved the "price margin" problem, it has failed to close the "quantity margin." Our findings identify a persistent reliance on peril-specific exclusions. This rationing is the primary mechanism insurers use to manage residual catastrophe and aggregation risk.

Insurers maintain these exclusions because Flood Re is not an "unlimited risk absorber." The scheme operates under strict statutory caps: a £3.2 billion annual liability limit and a £250 million loss limit. If losses exceed these thresholds, primary insurers remain liable to policyholders. Consequently, for the most exposed properties, insurers manage this tail risk by carving the flood peril out of the contract entirely.

"Moving from a low-risk to a high-risk postcode raises the probability of exclusion by approximately 37–40 percentage points."

This indicates that "affordability" has been achieved at the cost of "insurability." A policyholder may pay a standard market rate, but the policy often lacks the specific protection required for their geographic hazard.

5. Ex-Ante Hazard vs. Ex-Post Experience

We distinguish between "ex-ante" risk (mapped Flood Zones) and "ex-post" experience (recent flood events). While mapped hazard sets the baseline for exclusion, actual flood events trigger a severe "Experience Penalty." A local flood event in the 12 months prior to inception correlates with a 15-percentage-point increase in the probability of subsequent flood exclusion.

The following data demonstrates that the combination of high mapped risk and recent claims history renders a property nearly uninsurable in the private market.

Risk Indicators and Exclusion Probabilities

Property Risk Profile | Model-Implied Probability of Exclusion |

Not At Risk / No Previous Claim | 5.6% |

Not At Risk / Previous Flood Claim | 50.8% |

At Risk / No Previous Claim | 48.2% |

At Risk / Previous Flood Claim | 93.3% |

6. Market Heterogeneity and Insurer Strategy

Portfolio managers must account for significant variations in insurer behavior. While most incumbents (Insurers A, B, D, and E) transitioned toward premium convergence, "Insurer C" adopted an aggressive commercial strategy in the early 2020s. By offering discounted coverage in mapped flood zones to capture market share, Insurer C temporarily inverted the aggregate risk–premium relationship.

Strategic leads should view such inversions as commercial outliers rather than shifts in structural market equilibrium. When Insurer C is excluded from the data, the market-wide premium differential remains at a stable near-zero, confirming that the "discount" was a tactical maneuver rather than a sustainable repricing of climate risk.

7. The 2039 Sunset and Long-Term Sustainability

Flood Re is scheduled to exit the market in 2039, transitioning to fully risk-reflective pricing. However, the current framework's success in suppressing premiums has created "muted price signals," which may discourage necessary property-level adaptation. Without transparent price signals, the UK faces a "regressive climate retreat" where coverage collapses abruptly as the subsidy expires.

To secure a credible transition, our strategic recommendations include:

- Integrating Insurance Data in Land-Use: Utilizing exclusion patterns to inform planning and zoning decisions.

- Minimum Coverage Standards: Regulating the extent to which flood risk can be excluded from "standard" policies.

- Property-Level Resilience: Expanding the "Build Back Better" (BBB) endorsement, which provides up to £10,000 for resilient repairs, to reduce the underlying physical risk that insurers are currently rationing via the quantity margin.

8. Conclusion: Implications for Risk Management

The UK experience serves as a case study in the limits of subsidized reinsurance. While such schemes successfully stabilize the price margin, they route market discipline into less visible quantity rationing. The promise of universal insurability remains unfulfilled for the most exposed properties.

Without addressing contract terms, limits, and exclusions, the market risks a future where properties are "insured" by name but "rationed" by contract, leaving the most significant climate perils unmanaged and the underlying real estate collateral vulnerable.