Assessing the Structural Deficits of US Federal Flood Risk Management

Assessing the Structural Deficits of US Federal Flood Risk Management: A Comparative Governance Perspective

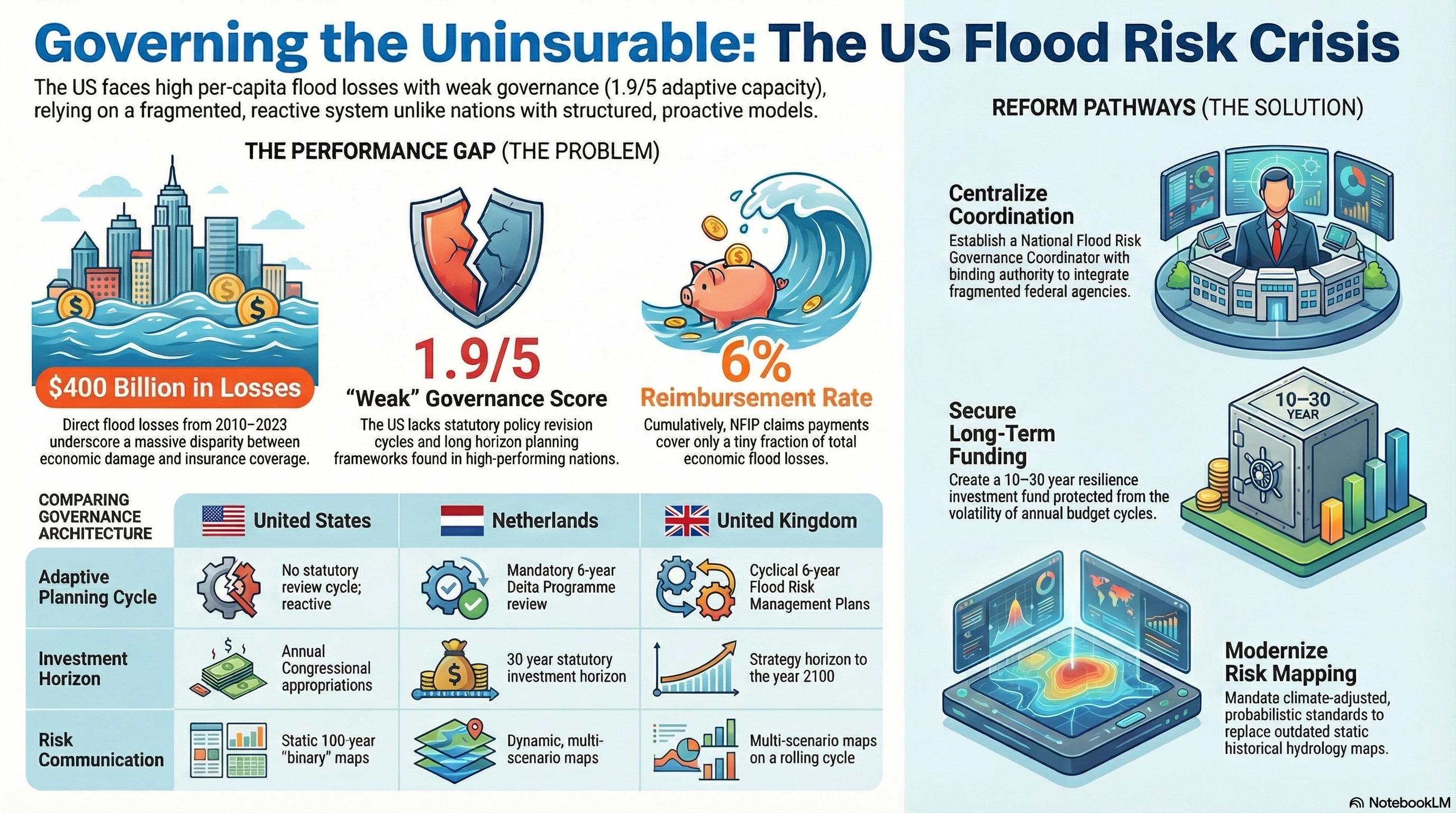

1. The State of US Flood Risk Governance

Empirical research conducted by Omoyeni (2025) indicates that the United States maintains the highest per-capita economic flood losses among industrialized nations. Despite the increasing frequency and severity of these events, the federal governance architecture has systematically resisted the structural adaptations observed in comparable OECD nations.

An assessment utilizing a multi-criteria adaptive governance framework assigned the US federal flood risk governance an aggregate score of 1.9 out of 5, a performance level categorized as "weak." This diagnostic identifies two primary institutional deficits as the drivers of this low score:

- Statutory Policy Revision Cycles: The absence of mandatory, scheduled periods to review and recalibrate governance frameworks based on evolving risk data.

- Long-Horizon Planning Frameworks: The lack of institutionalized planning mechanisms that extend beyond immediate disaster-driven timelines or short-term political cycles.

2. The Economic Disparity: Direct Losses vs. NFIP Indemnification

Synthesis of data from 2010 to 2023 highlights a profound "insurance gap," where the National Flood Insurance Program (NFIP) covers only a nominal fraction of total economic damages. This pattern suggests a structural architecture designed for post-disaster response rather than proactive risk pricing or reduction.

Table 1. Selected US Flood Loss Events and NFIP Claims Data, 2010–2023

Event | Direct Losses (USD Billion) | NFIP Claims Paid (USD Billion) |

2016 Louisiana Floods | 10.0 | 2.9 |

Hurricane Harvey (2017) | 125.0 | 8.9 |

2019 Midwest Floods | 12.5 | 0.4 |

Hurricane Ida (2021) | 75.0 | 1.6 |

Cumulative (2016–2023) | >$310.0 | ~$18.0 |

The 2019 Midwest floods are particularly illustrative of this gap, yielding a reimbursement rate of approximately 3.2%. This extreme disparity is attributed to the nature of the event-riverine flooding distinct from storm-surge events-which typically occurs in areas where insurance take-up is low and NFIP coverage is not mandated by lender requirements. Similarly, the reimbursement rate for Hurricane Harvey remained below 8%, underscoring the systemic underinsurance of US assets.

3. Theoretical Foundations: Adaptive Governance vs. Optimization

Adaptive governance scholarship (Folke et al., 2021) argues that in complex social-ecological systems defined by irreducible uncertainty, institutional effectiveness depends on the capacity to monitor and adjust rather than the ability to predict and optimize outcomes.

- Integrated Risk Management: Empirical analysis by Kreibich et al. (2022) demonstrates that governance systems investing in multi-actor coordination and integrated management protocols consistently produce lower impacts from subsequent events, even when those events are more severe.

- Institutional Fragmentation: While the US formally adheres to the principle of subsidiarity by distributing land-use authority to local governments, the lack of binding coordination mechanisms results in "institutional fragmentation" (Lukat et al., 2023). Without a robust capacity infrastructure to support local mandates, this formal distribution of power fails to produce coherent national risk outcomes.

4. Comparative Analysis: US vs. European Governance Models

Benchmarking the US against European frameworks reveals significant divergences in scale, planning horizons, and insurance architecture.

Governance Scale

- United States: Fragmented tiers across federal, state, and local levels lacking a unifying statutory coordination authority.

- Netherlands: Highly centralized; the "Delta Commissioner" holds statutory cross-sectoral authority and a clear national mandate under the Delta Act (2011).

- Germany: Federal-state (Länder) co-governance structured around river basin districts as mandated by the Federal Water Act (WHG).

- United Kingdom: Tiered statutory responsibility with "Lead Local Flood Authorities" (LLFAs) operating under the national oversight of the Environment Agency.

Planning Cycles

- United States: Characterized by a reactive, disaster-driven approach; NFIP reauthorization is subject to frequent lapses and lacks a statutory review cycle.

- Europe (Netherlands, Germany, UK): All three utilize mandatory six-year review cycles. The UK's strategy, anchored by the Environment Act (2021), includes a long-term horizon extending to the year 2100.

Insurance Architecture

- United States: A government-run, subsidized program (NFIP) with a cumulative debt exceeding $20 billion.

- United Kingdom: Utilizes "Flood Re" (Flood and Water Management Act 2010), a time-limited subsidy pool with a built-in risk-reduction pricing signal, scheduled for phase-out by 2039.

- Europe (General): Private-market dominant models where government backstops are reserved for extreme risks only, preventing public debt accumulation.

5. Diagnostic Taxonomy of US Institutional Barriers

Five principal barriers impede the development of adaptive capacity within the US federal system:

- Jurisdictional Fragmentation: Misaligned governance modes between federal mandates and local land-use authority prevent vertical and horizontal coordination.

- Annual Budgetary Cycle Mismatch: Dependence on annual Congressional appropriations creates a short-term political bias that undermines the long-term investment required for resilience.

- Static Risk Framework Reliance: Dependence on binary, historical hydrology (e.g., the 100-year floodplain) fails to account for dynamic, probabilistic climate scenarios.

- Moral Hazard in Federal Disaster Assistance: The availability of unconditional federal aid, coupled with "repetitive loss properties" receiving continuous federal coverage, reduces incentives for local enforcement of rigorous mitigation standards.

- Local Governance Capacity Deficits: Formal authority often rests with local entities that lack the technical and financial infrastructure to exercise that authority effectively.

6. Behavioral and Political Economy Dimensions

The interaction between subsidized premiums and unconditional disaster assistance creates an incentive architecture that discourages private investment in risk reduction (De Ruig et al., 2022b). Modeling suggests that transitioning the NFIP to risk-based premiums would generate a net societal benefit of approximately $10 billion. This benefit could rise to $26 billion if coupled with strategic regional protection investments.

The persistence of these subsidies is characterized not merely as a market failure, but as a "governance lock-in" driven by an informal institutional logic. This logic prioritizes the political economy of maintaining inaccurate actuarial rates over the fundamental restructuring required for long-term systemic stability.

7. Conclusion: Identified Reform Pathways

The findings of Omoyeni (2025) suggest that improving US flood risk outcomes requires a transition from programmatic adjustments to fundamental architectural reform. Proposed principles include establishing statutory planning cycles, protecting resilience investments from annual budget pressures, and developing the institutional "connective tissue" necessary for multi-level coordination.

These pathways align with Target E of the Sendai Framework for Disaster Risk Reduction 2015–2030, which emphasizes governance architectures capable of managing systemic risks. These insights provide a neutral framework for evaluating the durability of future federal climate resilience strategies and NFIP reauthorization debates.