One-Shot Individual Claims Reserving

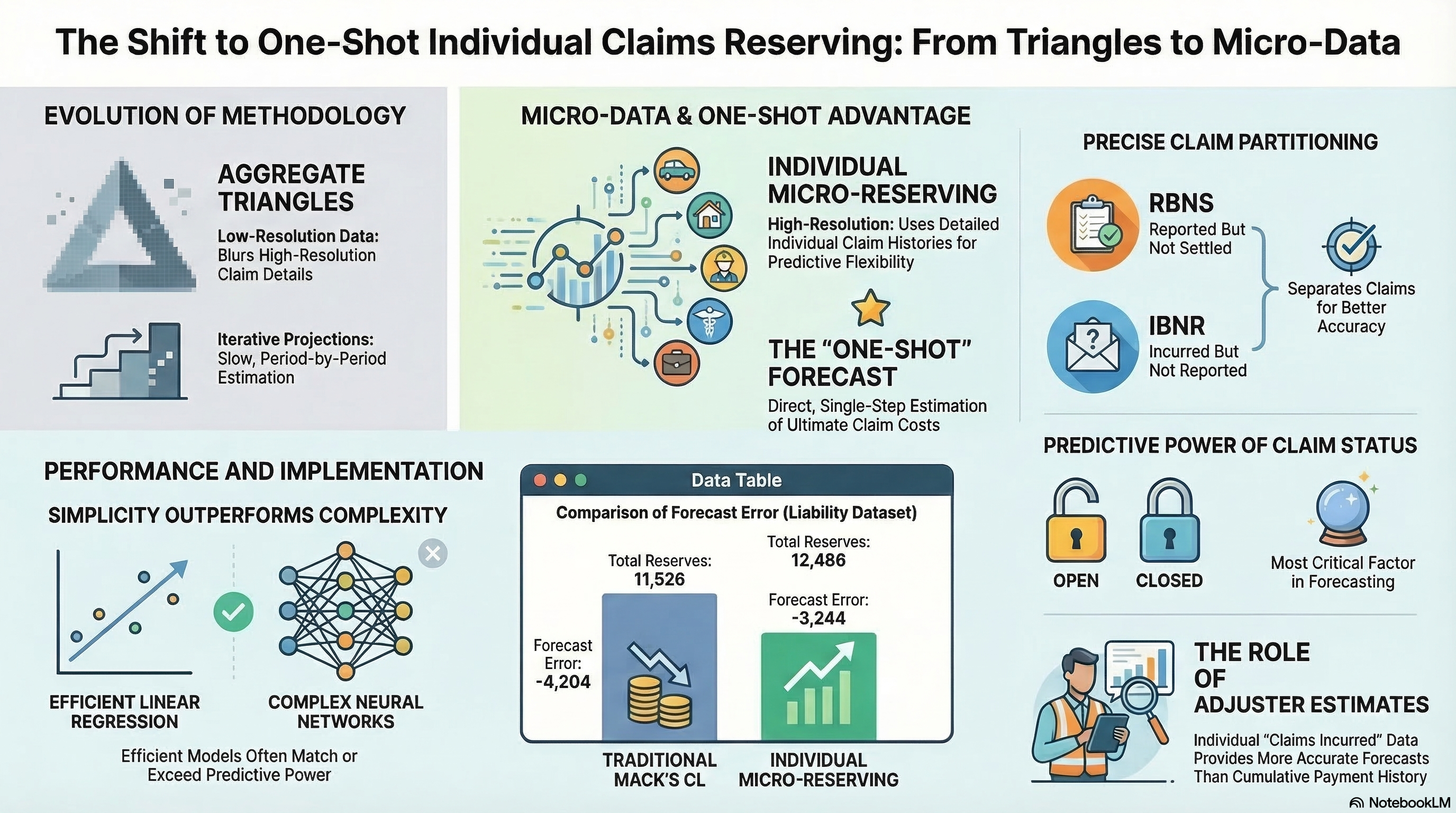

This research explores individual claims reserving, specifically focusing on the one-shot projection-to-ultimate (PtU) method as a modern alternative to the traditional chain-ladder approach. The authors demonstrate how to transition from aggregate data triangles to granular, claim-level modeling by directly estimating ultimate costs rather than using iterative year-over-year steps. This framework allows for the integration of stochastic covariates and machine learning techniques, such as neural networks and transformers, while maintaining a mathematical link to classical actuarial standards. The paper highlights a crucial decomposition of reserves into Reported But Not Settled (RBNS) and Incurred But Not Reported (IBNR) categories to ensure consistent claim cohorts. Through empirical case studies in accident and liability insurance, the text shows that linear regression often provides robust results for individual claims, effectively bridging the gap between simple aggregate methods and complex predictive modeling.